When you pick up a prescription at the pharmacy, you might not realize that the price you pay isn’t just about the drug-it’s about a hidden system called a formulary. Most employers in the U.S. offer health plans that include prescription drug coverage, and nearly all of them use formularies to decide which drugs are covered and how much you pay for them. The goal? Save money. And the easiest way to do that? Push you toward generics.

Generic drugs aren’t second-rate. The FDA says they’re just as safe and effective as brand-name versions. But they cost 80-85% less because manufacturers don’t need to repeat expensive clinical trials or run TV ads. That’s why your employer’s plan prefers them. In fact, generic medications save the U.S. healthcare system over $150 billion every year. That’s $3 billion a week. For your employer, that’s not just a cost-saving tactic-it’s a financial lifeline.

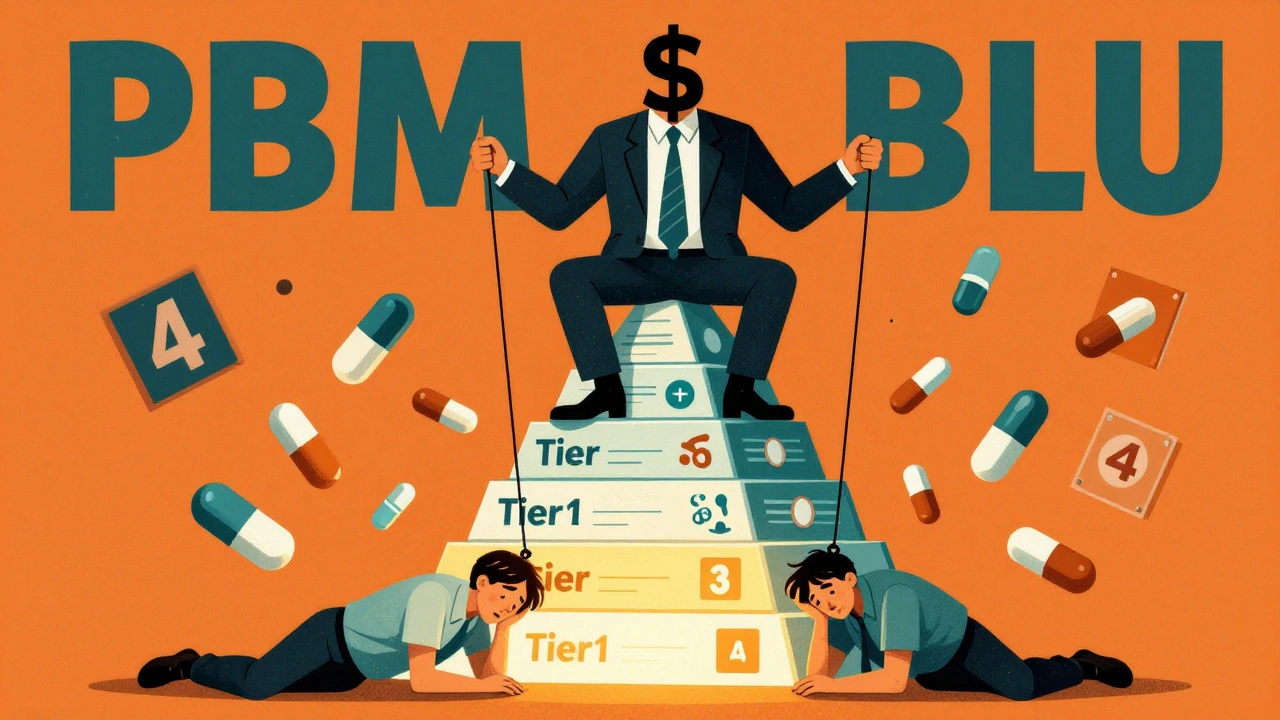

How Formularies Work: The Tiered System

Your employer’s drug coverage isn’t one flat rate. It’s broken into tiers. Think of it like a pricing ladder. The lower the tier, the less you pay.

- Tier 1: Generics - Usually $10 or less per prescription. This is where your plan wants you to be.

- Tier 2: Preferred brands - Brand-name drugs your insurer has negotiated a deal on. Expect $40 or so.

- Tier 3: Non-preferred brands - Brand-name drugs with no special deal. You’ll pay $75 or more.

- Tier 4: Specialty drugs - For complex conditions like cancer, MS, or rheumatoid arthritis. These can cost hundreds or even thousands per month.

Here’s the catch: if a brand-name drug becomes available as a generic, your plan will automatically move the brand version to Tier 4. Suddenly, the same pill you’ve been taking for years now costs seven times more. You’re not being punished-you’re being nudged. The system is designed to make the cheaper option the easiest one.

Who Controls Your Drug List? The PBMs

Behind the scenes, your employer doesn’t actually set the formulary. That’s handled by a Pharmacy Benefit Manager, or PBM. The big three-OptumRx, CVS Caremark, and Express Scripts-control prescription access for over 80% of Americans with employer-based insurance.

These companies don’t just manage claims. They decide which drugs get covered and which get kicked off the list. In January 2024, each of these three PBMs removed over 600 drugs from their formularies. That’s more than 1,800 medications gone in a single month. Why? To pressure drugmakers into offering bigger discounts.

It’s a game of leverage. If a drugmaker refuses to give a deep enough rebate, the PBM drops the drug. And if your medication gets dropped, you’re stuck paying full price unless you get an exception from your insurer. That’s not rare. It happens all the time.

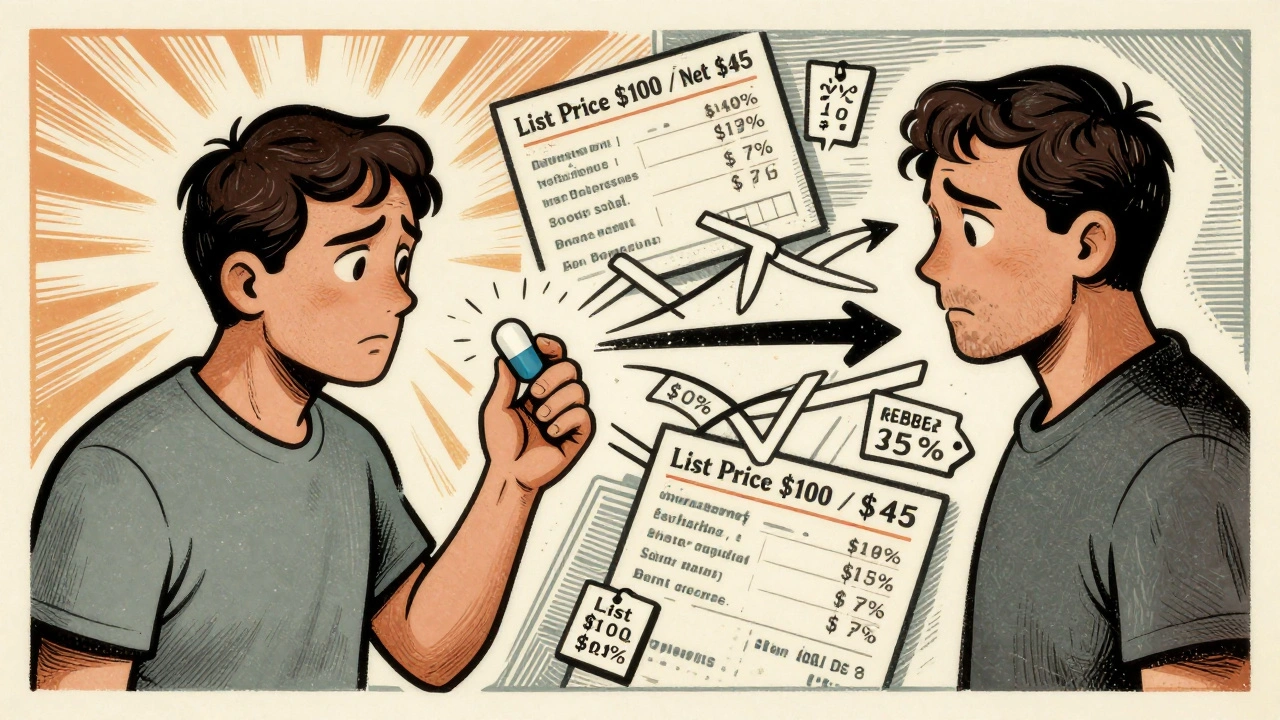

The Rebate Trap: Why Savings Don’t Always Reach You

Here’s the part no one talks about: the savings from generics and rebates don’t always end up in your pocket.

PBMs make money through something called gross-to-net pricing. That means the list price of a drug (what’s printed on the invoice) is way higher than what the PBM actually pays after rebates and discounts. On average, the difference is 55%. So if a drug costs $100 on paper, the PBM might only pay $45 after rebates. But guess what? You’re still charged based on that $100 list price.

That’s why you might see a $75 copay for a brand-name drug-even though the PBM paid only $30 for it. The gap between list price and net price is where PBMs make their profit. And unless your plan is designed to pass those savings along, you’re not seeing them.

What You Can Do: Navigate Your Coverage

You don’t have to accept whatever your plan throws at you. Here’s how to take control:

- Check your formulary - Go to your insurer’s website and search for your medication. Look for the tier it’s on. If it’s Tier 3 or 4, ask if a generic is available.

- Read your Summary of Benefits - This document, given to you during open enrollment, explains your drug costs. Don’t ignore it.

- Ask for a generic - Tell your doctor you’re open to a generic version. Most conditions can be managed just as well with generics.

- Request a formulary exception - If your drug was removed or moved to a higher tier, you can appeal. Your doctor can submit a letter explaining why you need it.

- Use in-network pharmacies - Some plans, like HealthOptions.org’s Price Assure Program, automatically lower your cost when you fill prescriptions at approved pharmacies.

Also, keep in mind: formularies change often. A drug that was covered last month might be gone this month. There’s no warning. That’s why it’s smart to check your coverage every time you refill a prescription.

Chronic Conditions and Special Programs

If you’re managing a long-term condition like diabetes, asthma, or high blood pressure, you might qualify for extra help. Some employers offer Chronic Illness Support Programs (CISP) that reduce out-of-pocket costs for ongoing medications. These programs often include free delivery, medication reminders, and one-on-one care coaching.

Don’t assume you’re on your own. Call your plan’s customer service and ask: “Do I qualify for any chronic condition support?” It’s a simple question that can save you hundreds a year.

Why Employers Push Generics-And Why It Matters

Employers aren’t trying to be stingy. They’re trying to survive. Health care costs have been rising for decades. Prescription drugs are one of the fastest-growing expenses. By steering employees toward generics, they can keep premiums lower and avoid cutting other benefits.

But there’s a flip side. Many employees don’t know generics are just as good. Some worry they’re weaker or made in sketchy factories. That’s not true. The FDA holds generics to the same standards as brand-name drugs. Same active ingredients. Same quality controls. Same safety checks.

That’s why smart employers are starting to educate their teams-through payroll inserts, email campaigns, and even text reminders. They’re not just changing formularies. They’re changing mindsets.

The Future: More Exclusions, More Transparency?

The trend isn’t slowing down. PBMs are getting more aggressive. Formulary exclusions are becoming a standard tool, not a last resort. And as drug prices keep climbing, employers will keep pushing for cheaper alternatives.

There’s growing pressure for transparency. Some states are starting to require PBMs to disclose how much of the rebate they keep. Congress is looking at capping the gross-to-net spread. But until then, you’re the one who has to figure out how to pay less.

The bottom line? Generics work. They’re safe. They’re cheaper. And if your plan pushes you toward them, it’s not because they don’t trust you-it’s because they’re trying to keep your coverage affordable. Your job? Understand the system. Ask questions. And don’t be afraid to switch to a generic unless your doctor says otherwise.

Are generic drugs really as good as brand-name drugs?

Yes. The FDA requires generic drugs to have the same active ingredients, strength, dosage form, and route of administration as the brand-name version. They must also meet the same strict standards for purity, stability, and performance. The only differences are in inactive ingredients (like fillers or dyes) and packaging. Generics are tested to ensure they work the same way in your body.

Why does my copay go up even when the drug hasn’t changed?

Your plan’s formulary changes. When a brand-name drug gets a generic version, the brand version is often moved to a higher tier-sometimes Tier 4-making it much more expensive. This isn’t a mistake. It’s intentional. The goal is to make the generic the default choice. Check your insurer’s website regularly for updates.

What if my medication was removed from the formulary?

You can request a formulary exception. Ask your doctor to write a letter explaining why you need that specific drug-maybe because generics didn’t work, or you had side effects. Submit it to your insurer. Many exceptions are approved, especially for chronic conditions. Don’t stop taking your medication while waiting-call your pharmacy to see if they can help you get a short-term supply.

Can I save money by switching to a different pharmacy?

Sometimes. In-network pharmacies often have negotiated prices that are lower than what you’d pay out-of-network. Some plans, like HealthOptions.org’s Price Assure Program, automatically apply discounts at specific pharmacies. Always check your plan’s list of preferred pharmacies before filling a prescription. You might save $20-$50 per fill.

Do PBMs pass savings on to employees?

Not always. PBMs earn money from the gap between the list price and the net price after rebates. That gap can be as high as 55%. Unless your employer’s plan is structured to pass those savings along, you won’t see lower copays-even though the PBM paid far less for the drug. Ask your HR department how your plan handles rebates. If they don’t know, it’s likely the savings aren’t being shared with you.

How often do formularies change?

All the time. PBMs update formularies monthly, sometimes weekly. A drug can be added, moved, or removed without notice. That’s why it’s important to check your coverage every time you refill a prescription. Don’t assume last month’s list still applies. Your plan’s website or member portal is the most up-to-date source.

Final Thoughts: Know Your Plan, Know Your Options

Employer health plans aren’t designed to confuse you. But they’re complicated by design-because complexity hides savings. The system favors generics not because they’re inferior, but because they’re smarter. And while PBMs control the rules, you still have power: you can ask questions, request exceptions, switch pharmacies, and choose generics when they’re available.

Don’t let the system run on autopilot. Take five minutes this week to log into your insurer’s website and look up your top three medications. See what tier they’re on. See if a generic exists. Ask your pharmacist if there’s a cheaper alternative. That small step could save you hundreds a year-and help keep your employer’s plan sustainable for years to come.

vanessa parapar

December 4, 2025 AT 02:18Okay but let’s be real-most people don’t even know what a formulary is until their $300 pill suddenly costs $800. I used to take Brand-X for my thyroid until my plan switched me to generic levothyroxine. Same pill, same effect, $12 copay. My doctor didn’t even blink. If you’re scared of generics, you’re scared of the FDA. And that’s just silly.

Ben Wood

December 5, 2025 AT 12:18Let’s not mince words: PBMs are predatory, profit-driven monopolies that exploit the illusion of cost-saving while extracting massive, opaque margins from patients. The gross-to-net pricing scheme isn’t a loophole-it’s a legalized heist. And don’t get me started on how OptumRx, CVS Caremark, and Express Scripts are all owned by the same corporate behemoths that also run your insurance, your pharmacy, and your EHR system. It’s a closed loop of exploitation-and you’re the pig.

Sakthi s

December 7, 2025 AT 11:22Generics work. Save money. Stay healthy. Simple.

Abhi Yadav

December 8, 2025 AT 10:06It’s not about the drug… it’s about the system that makes you feel like a burden just for needing to live. We’ve turned healthcare into a spreadsheet, and now we’re shocked when people break under the weight of it. The real tragedy isn’t the price tag-it’s that we’ve accepted this as normal. We’ve stopped asking why.

Julia Jakob

December 9, 2025 AT 19:29so like… pbms are basically the middlemen who charge you for the thing they’re supposed to be saving you money on?? and your employer doesn’t even know how it works?? i mean… why are we still letting this happen? i’m not mad… i’m just disappointed. like… we could fix this. but we don’t. because capitalism. sigh.

Robert Altmannshofer

December 9, 2025 AT 23:02Man, I used to be one of those people who’d refuse generics because I thought they were ‘inferior.’ Then I had a bad reaction to a brand-name blood pressure med-turned out the filler was triggering my allergies. Switched to generic. Zero issues. Cost me $5. My pharmacist said, ‘You’re lucky you didn’t get stuck with the non-preferred brand.’ That’s when I realized: this whole system is designed to confuse you into paying more. Knowledge is power. Check your formulary. Ask questions. Don’t just roll with it.

Kathleen Koopman

December 11, 2025 AT 10:24generics = ✅

pbms = 🤡

my wallet = 💸💸💸

my doctor = 😅

my insurance portal = 🤯

Nancy M

December 12, 2025 AT 19:15In many developing nations, generic medications are the backbone of public health infrastructure. The notion that they are somehow less reliable is a myth perpetuated by marketing, not science. The FDA’s equivalence standards are among the most rigorous in the world. If you trust your insulin, your antibiotics, your vaccines-all of which rely on generic production-you should trust your thyroid medication too. Cultural bias against generics is not grounded in pharmacology; it is rooted in perception, shaped by advertising and misinformation.

Precious Angel

December 14, 2025 AT 16:00Oh wow, so now we’re supposed to be grateful that our employers are forcing us onto cheaper drugs like we’re just… budgeting for groceries? Did you read the part where PBMs pocket 55% of the difference? That’s not saving money-that’s stealing it from your paycheck under the guise of ‘affordability.’ And don’t tell me generics are ‘just as good’-I’ve had two different generics for the same drug and one gave me migraines and the other made me nauseous. The FDA doesn’t test for how your body reacts to the fillers, just the active ingredient. So no. Not all generics are equal. And your employer doesn’t care. They just want to cut costs. And now you’re the guinea pig.

Krys Freeman

December 15, 2025 AT 00:34Why are we letting foreign factories make our meds? This is why America’s falling apart.

Jerry Ray

December 15, 2025 AT 09:01Wait-so if I’m on a brand-name drug that’s been around for 15 years and suddenly gets a generic, my plan moves the brand to tier 4? That’s not nudging. That’s sabotage. What if I’ve been on it for a decade and it’s the only thing that works? They don’t care. They just want to flip the switch and call it ‘cost-effective.’ This isn’t healthcare. It’s a rigged game.

David Ross

December 15, 2025 AT 12:52Let me be clear: the PBM model is not just unethical-it is structurally corrupt. The gross-to-net pricing mechanism is a deliberate obfuscation tactic designed to mask the true cost of drugs while inflating out-of-pocket expenses. This is not market efficiency. This is financial engineering at the expense of patient welfare. And the fact that Congress has not acted is a moral failure. The FDA approves generics. The courts should be holding PBMs accountable. But they’re not. And you? You’re paying for it.

Sophia Lyateva

December 16, 2025 AT 01:47you know what’s really happening? the government and big pharma are in cahoots. the generics? they’re all made in china and laced with microchips to track you. that’s why they’re cheaper-because they’re not really drugs. they’re surveillance tools. your insurance company knows when you take your pills. they’re selling your data. don’t fall for it. check your meds for RFID tags. i’m not joking.